Your choice of a first credit card is a big budgetary choice which can affect the way you spend, the credit score and the overall financial health in years to come. However, it is common among beginners to choose a credit card at random using what is advertised or whatever the banks offer without considering how the various cards meet various financial requirements. The result of this ignorant method is likely to be the selection of cards with interest rates that are high, fee imposition that is not necessary, or functionality that does not coincide with the pattern of real usage. Knowing how to analyze credit cards anew can help the novices choose the most appropriate card in their particular situation and have the best use of the rewards with minimal harm and risks.

Learning the Credit Card Basics

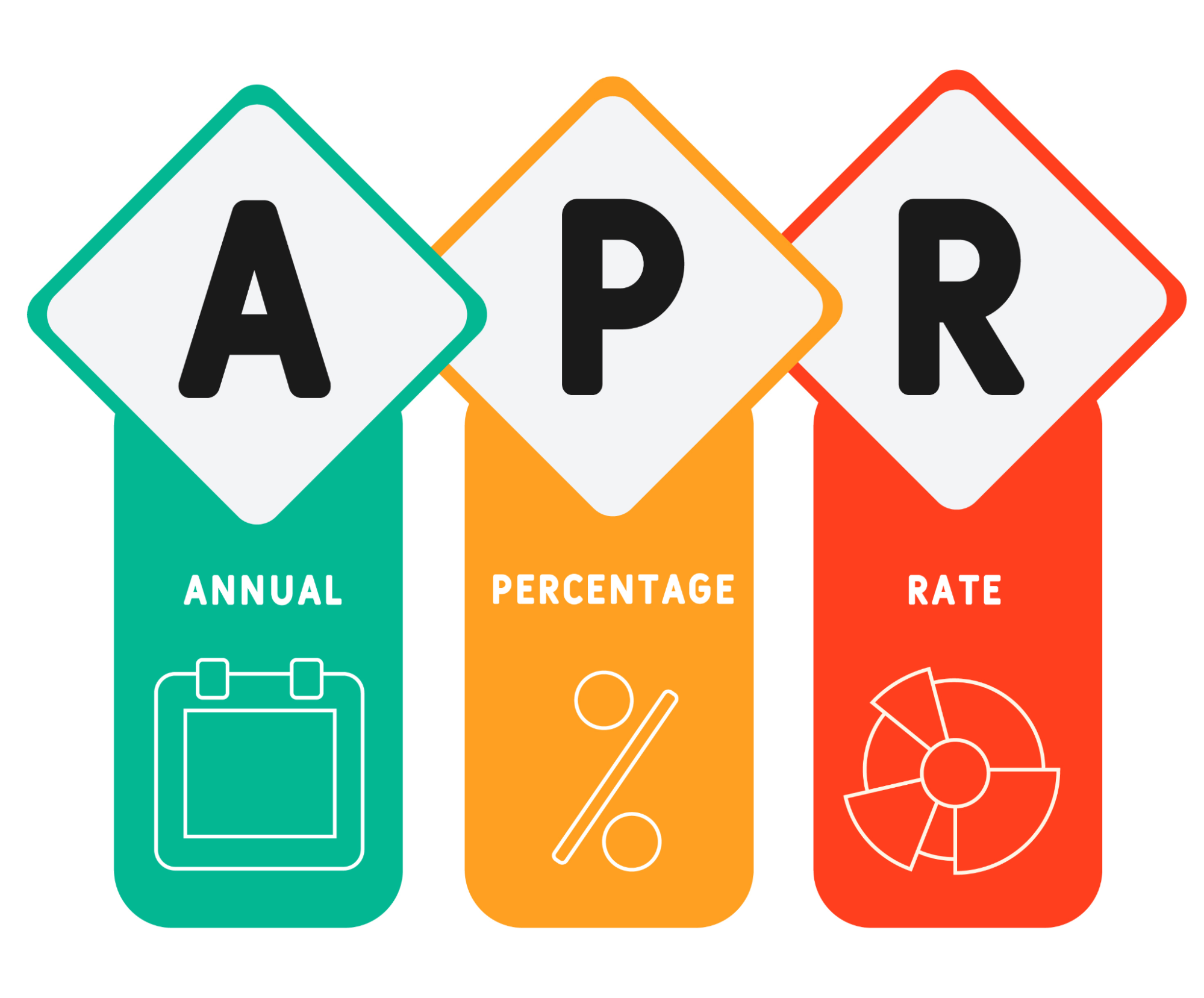

It is necessary to know fundamentals of credit card mechanics before comparison of specific cards. The next most costly item with credit cards is Annual Percentage Rate (APR), which is the interest rate on the carried balances. There are also extra costs in terms of annual fees, transaction fees, and foreign exchange fees depending on the type of card and usage. Rewards programs include cash back, traveling points or other reward on spending basis. Credit limits indicate the highest amount that you can borrow and minimum monthly payments involves paying at least part of the balance.

Most importantly, the choice of credit cards must be in line with your expected behavior. When you intend to pay all your balance in a month (never carry debt) then you need not worry about APR and rewards programs become relevant. When you expect to have balances in your account every now and then, the lowest APR is important than the highest rewards. Self-examination will help you to use the cards wisely since it is an honest appraisal of what you intend to use the card.

Assessing Card Choices in a Strategic Way

MoneyAtlas offers detailed credit card comparison and reviews that allow inexperienced users to compare choices in a systematic and not intuitive way. Compare cards on various fronts: APR rates, annual fees, rewards programs, sign-up bonuses, credit requirements and features that fit your lifestyle. A student who has a low amount of expenditure is likely to be not in need of a card that provides luxury when it comes to traveling. A business traveler who travels a lot may be more focused on travel rewards and lounge access in the airport despite the increased annual fees.

Credit Score Requirement and Odds of Approval

Various credit cards have varying credit scores that are to be qualified. The cards that focus on the excellent credit (760 and above) are usually associated with premium benefits and low APR. The mid-range cards consider good credit (670-759) with average rewards. Unsecured or secured cards assist in building credit with low income criteria and greater charges. Knowing the cards that will match your credit history will save you the hassle of wasting your time on cards that will not be approved–application will temporarily hurt your credit scores.

Eliminating Beginner Errors

Novices pursue welcome bonuses without considering the value maintained. Holding a card that benefits 50,000 bonus points is useless when the annual fees are bigger than redemption or when APR rates are disadvantageous when you carry balances sometimes. Some choose cards that have features that they do not need in their lives such as tracking business expenses when they do not own businesses. Premium cards with fees over $100/year will not be worthwhile until the benefits are more than the cost.

Starting Smart

One card that best suits your current credit profile and is intended to be used should be the starting point. Do not use several applications in a short period of time- an application will negatively impact credit scores temporarily, and a high number of applications in a short time is considered a sign of credit risk to a bank. Buy on installment and settle balances completely at the end of the month, which will leave a good credit record that will allow one to later have premium cards.

The Art of Credit Building

When you start with the right credit card, you can build up to a better financial carrying and credit record in your life, which allows you to choose better credit cards. Instead of performing the default to the one who is most aggressive in offering cards, consider your needs, compare and choose the card that is actually beneficial in your financial condition. This deliberate strategy will turn credit cards into an instrument of your financial ambitions as opposed to debt traps.